Before 2026, tax authorities had a blind spot when it came to crypto. If you bought Bitcoin in Japan, sold it in Canada, and held the cash in a Swiss bank account, there was no automatic system to connect those dots. That changed on January 1, 2026. The Common Reporting Standard got its biggest update ever - and crypto is now front and center.

What the CRS Actually Covers Now

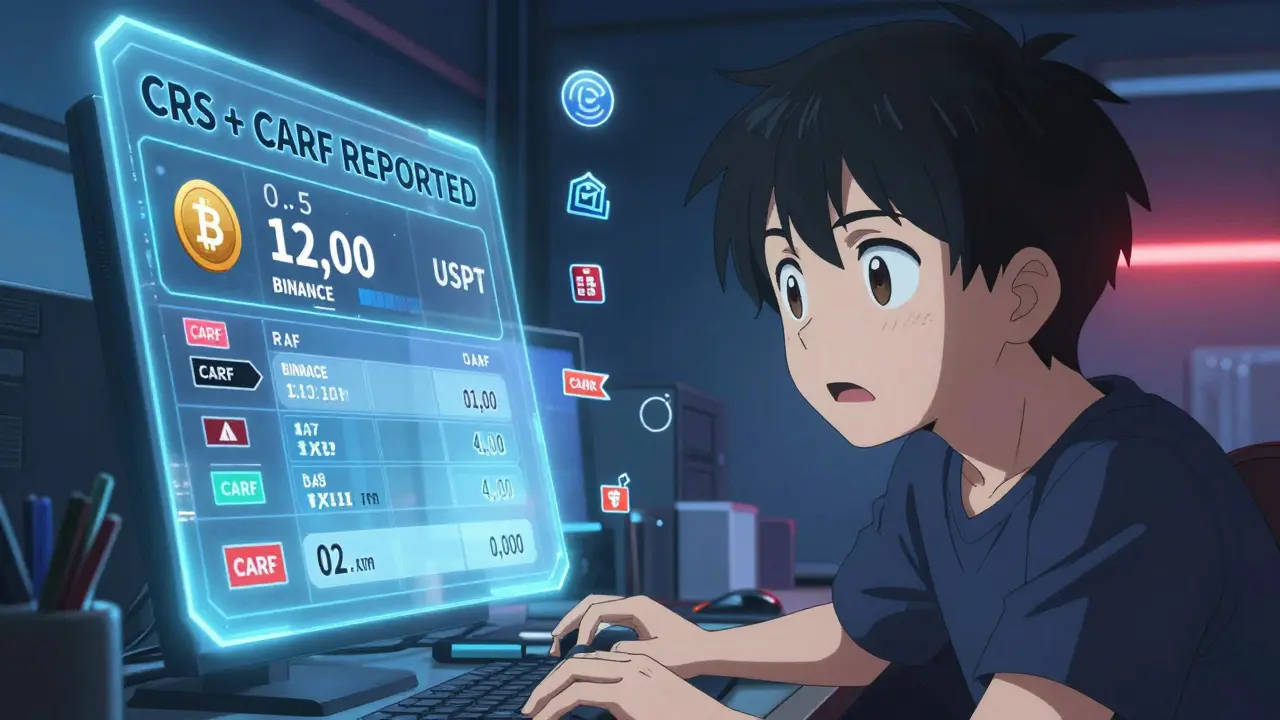

The Common Reporting Standard, or CRS, wasn’t built for crypto. It started in 2014 as a way for countries to share info about bank accounts, investment funds, and insurance policies held by foreign residents. Think of it as a global handshake between tax offices: if you’re a New Zealander with a Swiss bank account, Switzerland tells New Zealand about it - automatically, every year. But digital assets changed the game. Now, CRS 2.0 (the updated version effective January 1, 2026) includes crypto assets under its reporting umbrella. It doesn’t just track Bitcoin or Ethereum. It covers any digital representation of value that uses blockchain or similar tech to verify transactions. That includes stablecoins like USDT or USDC, crypto derivatives, and even certain NFTs if they’re used as investment vehicles. The key change? CRS now reports holdings. If you have $10,000 worth of Solana in a custodial wallet with a Swiss exchange, that exchange has to report it to Swiss tax authorities - who then send the info to New Zealand’s Inland Revenue Department. No need for you to file anything extra. The system does it for them.How CARF Works Alongside CRS

CRS doesn’t work alone anymore. It’s now paired with the Crypto-Asset Reporting Framework (CARF). While CRS looks at what you own, CARF tracks what you do - every trade, swap, or transfer between wallets or exchanges. For example: if you trade 0.5 BTC for 12,000 USDT on Binance, CARF requires the exchange to report that transaction. The report includes the value in local currency, the date, the parties involved (if identifiable), and whether it was a buy, sell, or swap. This data flows between tax authorities just like CRS data does. Think of it this way: CRS says, “You have this.” CARF says, “You moved this.” Together, they give tax agencies a full picture. No more hiding behind anonymous wallets or offshore exchanges - if the platform is regulated and reports under CARF, your activity is visible.Who’s Affected?

If you’re a resident of any of the 120+ countries that signed onto CRS, you’re affected. That includes New Zealand, the UK, the EU, Singapore, Australia, Canada, and most major economies. The rules hit financial institutions first. Banks, crypto exchanges, investment firms, and even some insurance companies must now:- Identify customers who are tax residents of other countries

- Track their crypto holdings (CRS)

- Report their crypto transactions (CARF)

- Update their KYC systems to flag crypto-related accounts

What Counts as a Reportable Crypto Asset?

Not every token gets reported. The OECD defines reportable crypto-assets as:- Coins and tokens traded on exchanges (Bitcoin, Ethereum, Solana, etc.)

- Stablecoins pegged to fiat currencies (USDT, USDC, DAI)

- Crypto derivatives (futures, options, leveraged tokens)

- NFTs that function as investment assets - like fractionalized real estate NFTs or royalty-bearing digital art

How This Changes Your Tax Obligations

You’ve always been required to report crypto gains on your tax return. But now, tax authorities have proof. If you sold Bitcoin in 2025 for a $50,000 profit and didn’t declare it, the IRS or IRD will know - because the exchange reported it. This isn’t about new taxes. It’s about enforcement. The system now has the data to catch people who used to slip through the cracks. In New Zealand, crypto gains are taxable as income or capital gains depending on intent. In the UK, you pay Capital Gains Tax. In the EU, it varies by country, but all are aligning under DAC8 - the EU’s version of CARF. The bottom line: if you made money from crypto, you’re now far more likely to be caught if you didn’t report it. The days of assuming “no one will know” are over.

Implementation Is Patchy - But Getting Tighter

Not every country rolled out CRS 2.0 and CARF on January 1, 2026. Some, like Guernsey and the UK, were ready. Others are still drafting laws. The EU is implementing through DAC8, which takes effect in 2027. The US hasn’t formally adopted CARF, but major exchanges like Coinbase and Kraken are already reporting under CRS rules because they operate globally. This creates a tricky situation. If you’re a New Zealander using a US-based exchange that doesn’t report under CARF, your data might still be reported under CRS. But if you use a small, unregulated exchange based in a non-CRS country, you might fly under the radar - for now. Experts warn that this gap won’t last. The OECD is pushing for universal adoption. Countries that don’t comply risk being blacklisted, which means their financial institutions lose access to global banking networks. So even if your country is slow, the pressure to join is intense.What You Should Do Now

Don’t wait for a letter from the tax office. Here’s what to do:- Review your crypto activity from 2024 and 2025. Did you sell, trade, or earn crypto? If yes, you likely owe tax.

- Use tax software that supports crypto (like Koinly, CoinTracker, or CryptoTaxCalculator). These tools now pull data directly from exchanges via API - including CRS-reported info.

- If you held crypto on non-custodial wallets, keep detailed records: dates, amounts, values in NZD at time of transaction.

- Don’t ignore past years. Many tax agencies are running amnesty programs for voluntary disclosures before audits ramp up in 2027.

What’s Next?

This is just the beginning. The OECD is already working on the next phase: reporting DeFi transactions, NFT marketplaces, and staking rewards. By 2028, even decentralized protocols might be forced to report through their service providers. The message is clear: crypto isn’t anonymous anymore. The global tax system has adapted. The tools are in place. The data flows automatically. The only thing left is for you to get your records in order.Does CRS report every crypto transaction I make?

No. CRS reports holdings - not every trade. It tells your home country what crypto assets you own through regulated platforms. CARF handles transactions, like buying, selling, or swapping crypto. But only if you use a platform that reports under CARF. If you use a non-custodial wallet and never touch a regulated exchange, your transactions won’t be reported - yet.

I use Coinbase. Do they report my crypto to New Zealand?

Yes. Coinbase is a CRS-reporting institution. If you’re a New Zealand tax resident, they report your crypto holdings and transaction data to the New Zealand Inland Revenue Department (IRD) through the automatic exchange system. This started in 2026 under the updated CRS and CARF rules.

What if I didn’t report crypto gains in past years?

Many tax agencies, including New Zealand’s IRD, offer voluntary disclosure programs. If you come forward before an audit, you may avoid penalties or prosecution. The sooner you correct past filings, the better. Waiting increases your risk - especially now that CRS and CARF are active.

Are NFTs included in CRS reporting?

Only certain NFTs. If an NFT functions as an investment - like a fractionalized real estate token or a digital artwork sold for profit - it’s reportable. Personal-use NFTs, like profile pictures or game items, are generally excluded. The key is whether the asset has market value and is held for investment purposes.

Does CARF apply to decentralized exchanges (DEXs)?

Not directly. CARF targets regulated financial institutions - not decentralized protocols. But if you use a DEX through a centralized platform (like MetaMask connected to a KYC’d wallet on a regulated exchange), that platform may report the transaction. As of 2026, DEXs themselves aren’t required to report - but regulators are working on ways to close that gap.

Santosh kumar

February 13, 2026 AT 09:54Just read this and felt a wave of relief. I’ve been holding onto some BTC from 2023 in a custodial wallet and was stressing about past trades. Knowing the system is now automated makes me want to finally clean up my records. No more guessing games.

Claire Sannen

February 13, 2026 AT 20:46This is actually one of the most thoughtful breakdowns I’ve seen on crypto taxation. The CRS+CARF combo isn’t perfect, but it’s a massive step toward fairness. People who thought they could hide behind decentralized wallets need to wake up - the infrastructure is catching up. And yes, Koinly and CoinTracker are lifesavers for non-experts like me.

Christopher Wardle

February 14, 2026 AT 20:49Interesting how the system evolved. CRS was never meant for crypto. Now it’s a bridge between old financial transparency and new digital reality. The real question isn’t whether it works - it’s whether governments will use the data responsibly. Surveillance isn’t the goal. Equity is.

Holly Perkins

February 15, 2026 AT 16:38i dont even know if i should care anymore like i sold like 3 btc in 2022 and forgot about it lol

Will Lum

February 17, 2026 AT 08:37Been holding for years and never filed anything. Guess I’m not the only one who thought no one was watching. Turns out they were. Just glad I found this before the audit letters start rolling in. Time to pull up my old transaction logs and get it sorted.

Sanchita Nahar

February 18, 2026 AT 14:11So basically if you used any exchange you’re screwed now? No more hiding? What a joke. They’re just trying to squeeze more money out of people who actually built this space

Ben Pintilie

February 19, 2026 AT 14:54Yikes. I had like 50 ETH in a wallet on Binance in 2024. I didn’t report it. Guess I’m gonna be one of those ‘voluntary disclosure’ stories now 😅

Sakshi Arora

February 21, 2026 AT 06:17so carf tracks trades but not if you use metamask right like what if i just swap tokens on uniswap

bala murali

February 23, 2026 AT 05:41The alignment of CRS and CARF represents a paradigm shift in global fiscal governance. The convergence of sovereign reporting obligations with decentralized asset verification mechanisms necessitates a recalibration of tax compliance frameworks. This is not merely regulatory expansion - it is structural integration of digital capital into the international fiscal order.

Kaz Selbie

February 23, 2026 AT 08:38Oh so now even people in India and Brazil are gonna get reported on? That’s hilarious. Most of them don’t even file income tax. How’s that gonna work? This whole system is built on a fantasy of global compliance. It’s not scalable.

SAKTHIVEL A

February 25, 2026 AT 04:06Let me be clear: this is not transparency. This is financial colonization. The OECD, dominated by Western powers, has weaponized accounting standards to impose their fiscal doctrine on emerging economies. The very notion that a New Zealander’s crypto activity must be reported to a Swiss institution is colonialism dressed as regulation.

Who authorized this? Who voted on it? The global south was never consulted. This is a quiet coup - executed through compliance forms and API integrations.

And now they’re coming for DeFi? Next they’ll demand that smart contracts submit quarterly tax returns. Absurd. This isn’t progress. It’s control.

Tammy Chew

February 26, 2026 AT 08:00OMG I just realized I’ve been holding NFTs that are technically reportable?? Like that one Bored Ape I bought for 10 ETH? I thought it was just a fun profile pic 😭

Wait does this mean I owe taxes on my cat NFT too??

Lindsey Elliott

February 27, 2026 AT 03:24Wait so if I didn’t report my 2023 gains and now they’re coming through CRS, does that mean I’m gonna get audited?? I’m literally gonna have a panic attack

Beth Trittschuh

February 28, 2026 AT 02:23There’s something deeply poetic about crypto’s journey - from anonymous peer-to-peer experiment to a regulated asset class tracked by global tax authorities.

We wanted decentralization. We got interconnectivity.

We wanted freedom from banks. We got compliance with banks.

Maybe the real revolution wasn’t the technology. Maybe it was the realization that no system, however decentralized, can escape the gravity of human institutions.

And yet… here we are. Still holding. Still trading. Still believing.

Benjamin Andrew

February 28, 2026 AT 18:18While the structural implementation of CRS 2.0 and CARF represents a significant advancement in transnational fiscal accountability, it is imperative to acknowledge the asymmetrical burden placed upon retail participants versus institutional actors. The regulatory architecture, while technically robust, fails to account for the cognitive dissonance experienced by individuals who engaged with crypto under the assumption of operational anonymity. This constitutes a retroactive imposition of compliance obligations - a legal and ethical grey zone that demands legislative remediation, not merely enforcement.